Crafting Non Fungible Excellence

Delivering Web3 Strategic Objectives

We turbocharge your business’s transition to Web 3 with our 15+ years of experience, supported by over 1000 experts and with track record of 1200+ successful enterprise implementations

Driving Ingenuity with Relentless Blockchain Innovation

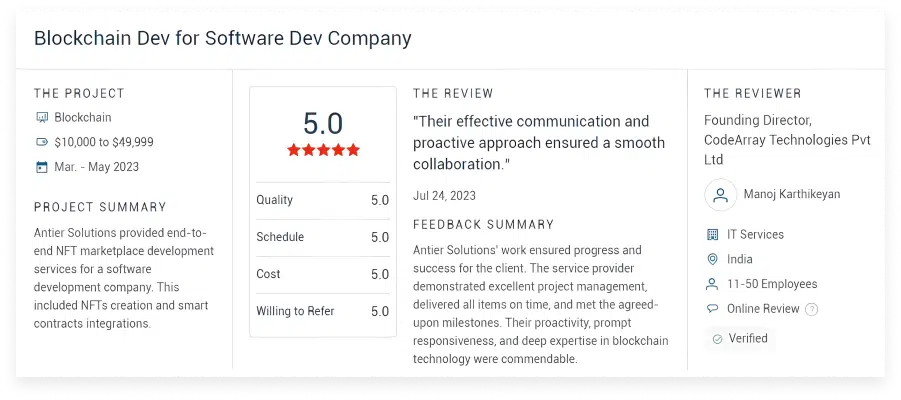

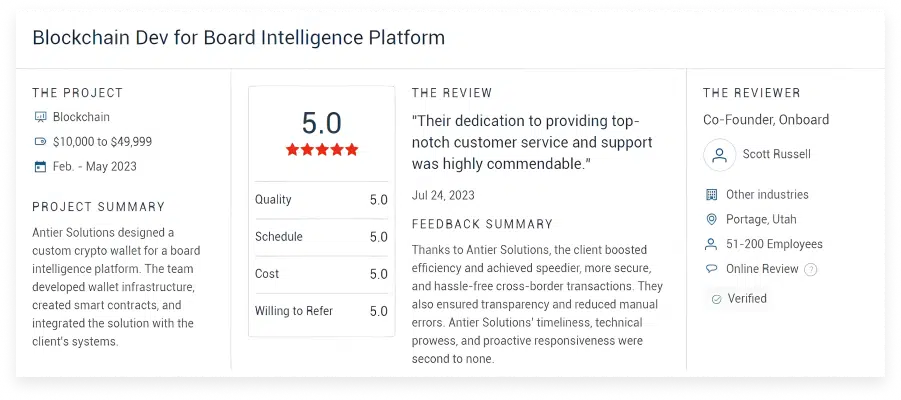

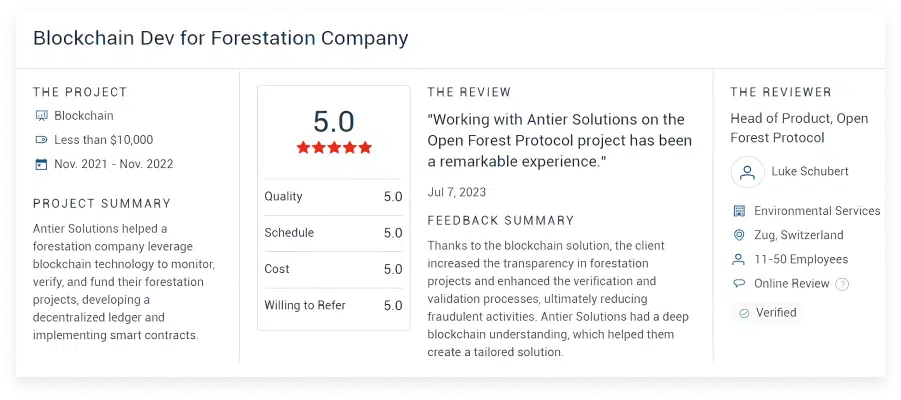

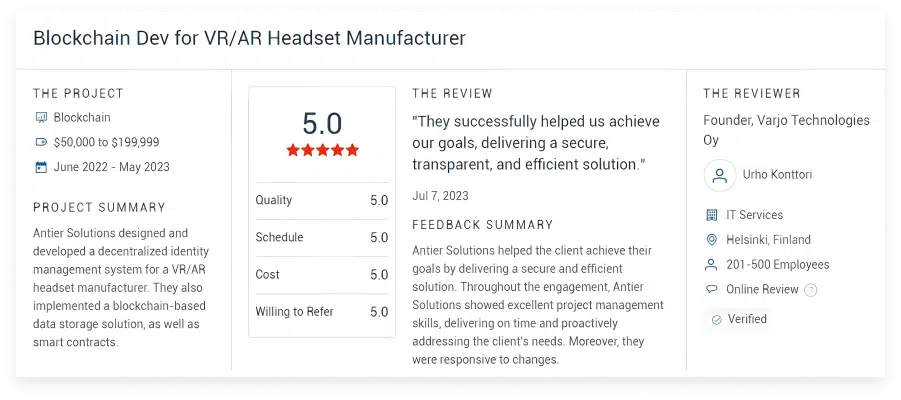

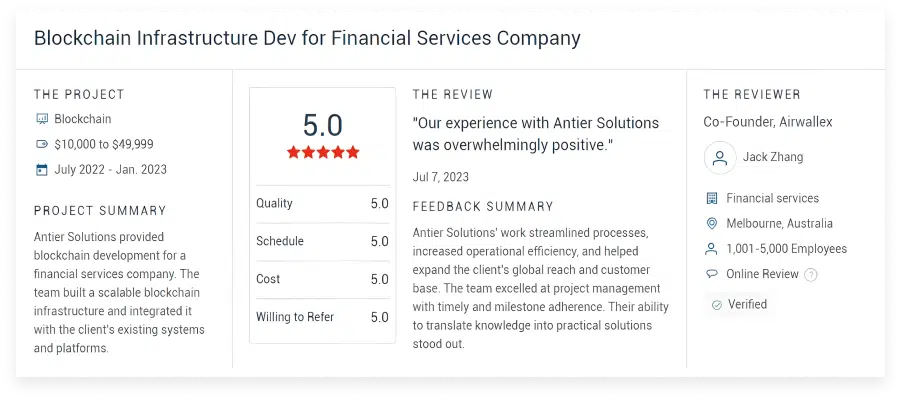

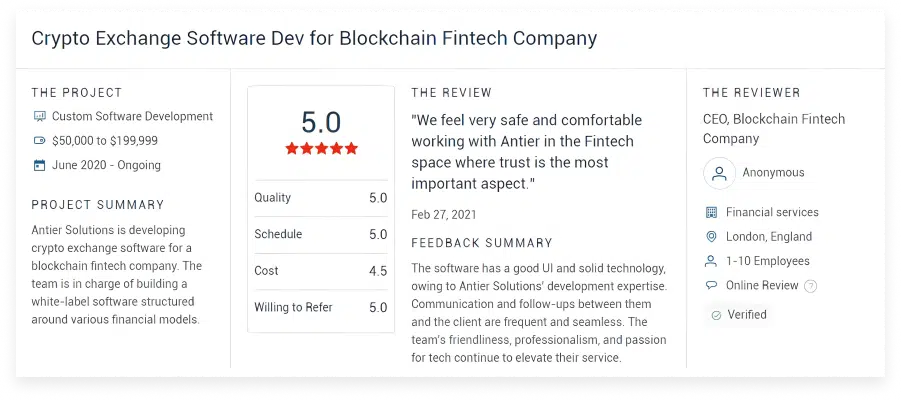

What Clients Say